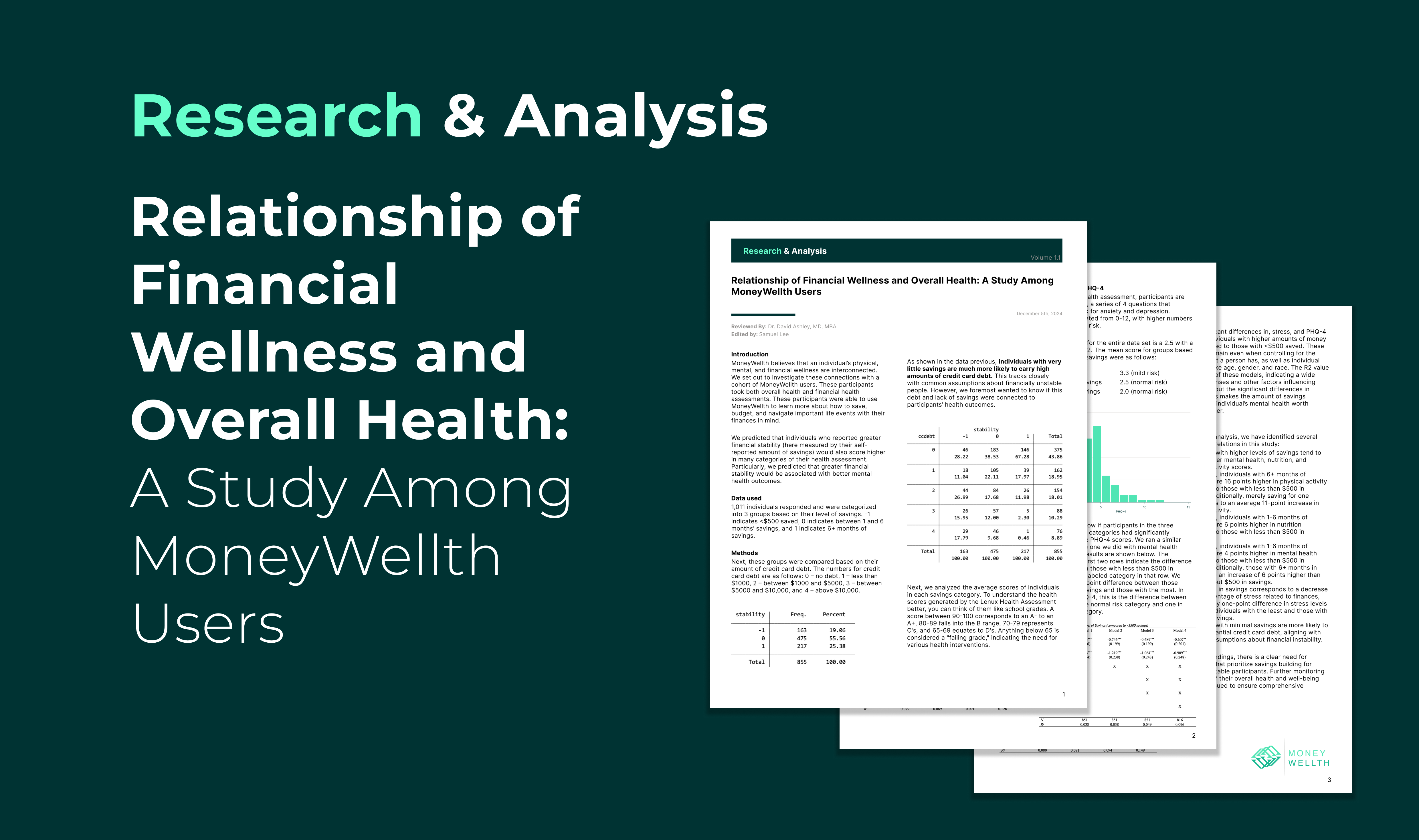

Financial wellness is often framed as achieving personal goals or escaping debt, but its ties to physical and mental health are profound. At MoneyWellth, we explored this connection in a study of over 1,000 participants, uncovering surprising insights into how financial behaviors influence well-being.

Key Findings: The Link Between Savings, Debt, and Health

Participants in our study were grouped based on their savings levels:

- Less than $500 saved

- 1-6 months of savings

- Over six months of savings

We analyzed their mental health, physical activity, nutrition, and stress levels. The results were striking:

- Mental Health: Participants with less than $500 in savings scored, on average, four points lower in mental health assessments compared to those with moderate savings. Those with over six months of savings scored six points higher—enough to move from “mild risk” to “normal risk” for anxiety and depression.

- Physical Activity: Those with over six months of savings scored 16 points higher in physical activity metrics than individuals with minimal savings. Even a one-month savings buffer provided an 11-point boost.

- Stress and Coping: Financial stress was overwhelmingly higher in participants with less than $500 in savings, making up nearly 100% of their reported stress. In contrast, those with greater savings reported much lower financial stress.

A surprising finding was that while high debt levels negatively impacted mental health, the absence of savings had an even greater impact on overall health outcomes. This suggests that focusing on savings—not just reducing debt—can be a more immediate and impactful path to improved well-being.

The State of Financial Wellness in America

In the United States, nearly 60% of adults live paycheck to paycheck, and 40% have less than $500 in emergency savings. Meanwhile, credit card debt is at a historic high, with the average household carrying over $6,000 in balances. Beyond the numbers lies a deeper cultural shift tied to Shifting Baseline Syndrome (SBS)—a phenomenon where each generation normalizes progressively worsening conditions. In this case, debt has become an accepted part of life, making the absence of savings feel even more destabilizing. This normalization masks the compounded stress and health impacts of financial insecurity, which our research reveals in stark detail.

Why Does Financial Stability Matter for Health?

The normalization of debt through SBS has dulled our awareness of its cascading effects. Chronic financial stress—whether from debt or lack of savings—creates biological responses that harm physical and mental health. Without a safety net, every unexpected expense becomes a crisis, perpetuating cycles of poor health choices and stress.

On the other hand, even modest savings reduce this stress, fostering healthier habits and better coping mechanisms. Building a financial buffer, no matter how small, helps break this cycle, offering a pathway to resilience and stability.

What Does This Mean for You?

Our findings emphasize that financial wellness isn’t just about managing debt—it’s about prioritizing savings. Starting small, even with as little as $10, can have profound effects:

- Reducing financial stress

- Encouraging healthier lifestyle choices

- Improving mental health outcomes over time

A Call to Action: Prioritize Budgeting and Saving

At MoneyWellth, we’re committed to dismantling the barriers to financial equity. Through tools like budgeting simulations and savings challenges, we empower individuals to take control of their financial futures.

If you feel stuck or overwhelmed by your finances, remember: small steps today can lead to significant change tomorrow. Reclaim your financial wellness, your health, and your peace of mind.

Let’s build a future where financial wellness isn’t an aspiration but a foundation for a healthier, happier life. Start your journey with MoneyWellth today.